Erdgas deckt etwa ein Viertel des gesamten Energiebedarfs in Österreich. 80 Prozent davon kommen aus Russland. Industrieunternehmen mit hohem Gasbedarf können kaum auf diese Energiequelle verzichten. Was also passiert, wenn Russland wirklich den Gashahn ganz zudreht? Und wie ist es derzeit um die Gasversorgung in Österreich bestellt?

Aktuelle Gas-Situation in Österreich

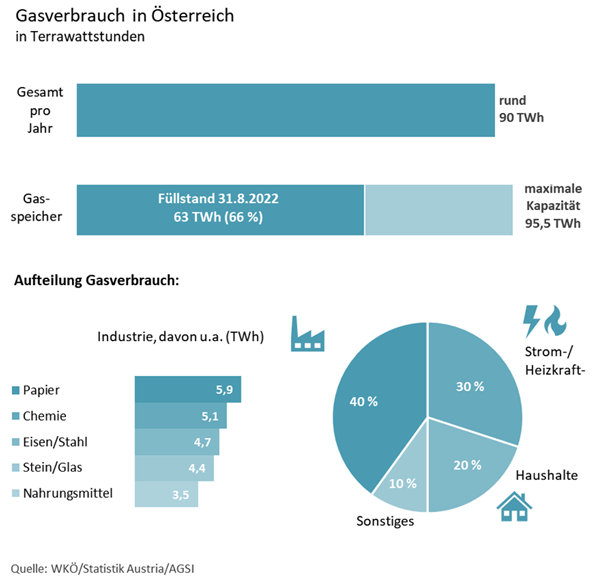

Österreich verbraucht jährlich knapp 90 Terawattstunden (TWh) Erdgas. Rund zehn Prozent dieser Menge werden durch inländische Produktion abgedeckt. Gefördert wird dieses Gas durch die

OMV und

RAG Austria. Der Rest wird importiert, bis ins Jahr 2022 hinein zu 80 % aus Russland. Ob der russische Importanteil inzwischen tatsächlich auf 50 % reduziert wurde oder

sogar noch zugenommen hat, darüber herrscht derzeit in Österreich Uneinigkeit.

Notfallplan trifft vor allem Unternehmen

Falls es zu einem Lieferstopp russischen Gases als Reaktion auf die westlichen Sanktionen kommt, kann der Staat

Energielenkungsmaßnahmen ergreifen, damit bevorzugt Haushalte und soziale Einrichtungen wie Krankenhäuser, Altenheime und Kindergärten versorgt werden können. Auch systemrelevante Verbraucher wie Nahrungsmittelindustrie, Treibstoffindustrie, Holzindustrie oder Energieerzeugungsanlagen dürfen ausgenommen werden.

Die Kehrseite des Notfallplans: Für Industrie und Gewerbe wird es noch viel enger, als es ohnehin schon heute ist. Bleibt das Gas komplett aus, müssten zunächst 35 große österreichische Industrieunternehmen mit hohem Gasverbrauch ihre Produktion einschränken. Sofern dies nicht ausreicht, kommen weitere 7.500 Unternehmen hinzu, deren Gasverbrauch mehr als 400.000 Kilowattstunden jährlich übersteigt.

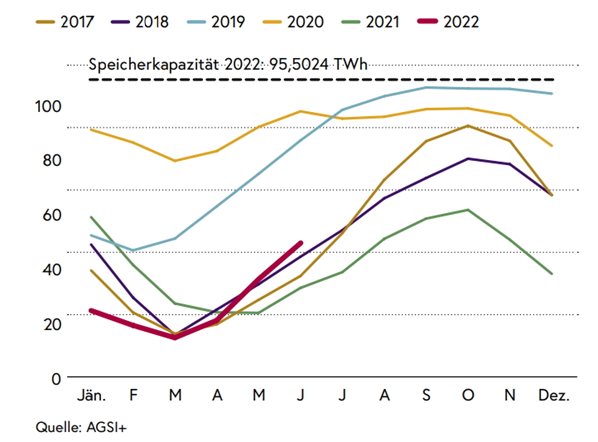

Wie einschneidend die Maßnahmen werden könnten, hängt vor allem vom Füllstand der Gasspeicher ab und inwieweit Gas aus anderen Ländern als Russland beschafft werden kann.

Gasspeicher füllen sich zunehmend

Die österreichischen Gasspeicher sind mittlerweile mit 63 TWh Erdgas aufgefüllt – das entspricht einem Füllstand von 66 Prozent (31.8.2022,

aktuelle Füllstände siehe AGSI+). Die Speicher der OMV sind zu 91 Prozent voll. Die Speichermenge entspricht somit knapp drei Viertel des Jahresverbrauchs in Österreich. Allerdings besteht lediglich auf die strategische Reserve von 20 TWh voller Zugriff.

Die Grafik zeigt die Füllstände im Jahresverlauf im Zeitraum 2017 bis 2022. Das Jahr 2020 ist pandemiebedingt aufgrund des geringeren Gasverbrauchs nicht repräsentativ. Die geringen Speichermengen im zweiten Halbjahr 2021 sind eine Folge der seit Mitte 2021 stark gestiegenen Großhandelspreise für Gas. Mit dem Ausbruch des Ukraine-Krieges im ersten Quartal 2022 hat sich die Situation verschärft (

Quelle: Energie in Österreich 2022, AGSI+).

Die Mär vom hohen Gasverbrauch privater Haushalte

Der Energieverbrauch der Haushalte nimmt keine so wichtige Rolle ein wie allgemein angenommen. In den vergangenen Jahren ist der Gasanteil zur privaten Energieversorgung auf unter 20 % im Energiemix gesunken.

.png.aspx?width=599&height=307)

Weitere 10% werden für Verkehr, Dienstleistungen und sonstiges aufgewendet. 30% der gesamten Gasnachfrage wird im Umwandlungsbereich für die Strom- und Fernwärmeerzeugung eingesetzt und dient vor allem der Stabilisierung des Stromnetzes (Kraftwerke, Heizkraftwerke, Fernheizkraftwerke).

Der Hauptanteil des Erdgases geht mit rund 40 % in die produzierende Industrie, als Rohstoff oder zur Erzeugung von Prozesswärme – und zwar auch im Sommer. Die Industrie in Österreich ist somit in hohem Maß von Erdgas abhängig. Vor allem die Stahl-, Papier-, Glas- und Chemiebranche benötigt große Mengen.

2020 betrug der Energetische Endverbrauch bei Papier und Druck 5,9 TWh Gas, in der Chemie und Petrochemie waren es 5,1 TWh. Das entspricht 19,3 bzw. 16,7 Prozent des gesamten Gasverbrauchs im produzierenden Sektor. Dahinter folgen die Eisen- und Stahlerzeugung mit 4,7 TWh Gas, die keramische Industrie (Steine und Erden, Glas) mit 4,4 TWh und die Lebensmittelindustrie mit 3,5 TWh.

Die unbequeme Wahrheit: Es gibt keine kurzfristige Alternative zu Erdgas

Österreichs Abhängigkeit von Gasimporten ist über Jahrzehnte gewachsen und aufgrund fehlender Infrastruktur weder mit Biogas, LNG-Flüssiggas, Wasserstoff oder alternativen Energien kurzfristig veränderbar. Auch die Umstellung auf Kohle oder Öl ist nur in geringem Ausmaß möglich.

Die österreichische Wirtschaft kann ohne Erdgas nicht aufrechterhalten werden. Insbesondere in der produzierenden Industrie ist Erdgas derzeit alternativlos. Wird der kontinuierliche Nachschub an Gas unterbrochen, muss die Produktion eingeschränkt oder - wo das nicht möglich ist - heruntergefahren werden. Solche Abschaltvorgänge großer Anlagen dauern Wochen und sind sehr kostenintensiv. Hinzu kommen Produktionsengpässe in nachgelagerten Branchen aufgrund der Komplexität der Wertschöpfungsketten.

So einfach ist das Herunterfahren der Industrie eben nicht, ganz zu schweigen von den Schäden an Produktionsanlagen bei einem Totalausfall der Gaszufuhr. In der Stahlindustrie, bei der Herstellung von Glas und in Gießereien würde ein Gasstopp zu einem Komplettausfall der Schmelzprozesse führen und irreparable, millionenteure Schäden an den Produktionsanlagen verursachen.

Ebenso würde die Herstellung von pharmazeutischen Produkten zum Erliegen kommen. In der

Halbleiterproduktion sowie bei der Herstellung von Hygieneprodukten und Verpackungen wären irreparable Schäden an den Anlagen die Folge, die ein Wiederhochfahren in kurzer Zeit unmöglich machen.

Lebens- und Düngemittelindustrie: 70 % weniger Düngemittel

Erdgas wird in allen Bereichen der Lebensmittelproduktion benötigt, da viele Produktionsschritte sehr energieintensiv sind oder sehr hohe Temperaturen benötigen. Kaum ein Produzent von Lebens- und Futtermitteln oder Getränken kommt derzeit ohne den fossilen Energieträger aus.

So treibt Gas beispielsweise Getreide- und Ölmühlen an und wird benötigt, um Kühlketten z.B. bei Molkereiprodukten aufrechtzuerhalten. Ein Gas-Lieferstopp würde die Versorgungssicherheit in Österreich gefährden. Kommt aus der Pipeline kein Gas, steht die Lebensmittelproduktion.

Doch auch ohne Gasstopp ist die Situation im Nahrungsmittelbereich bereits enorm angespannt. Die hohen Erdgaspreise haben die Preise für

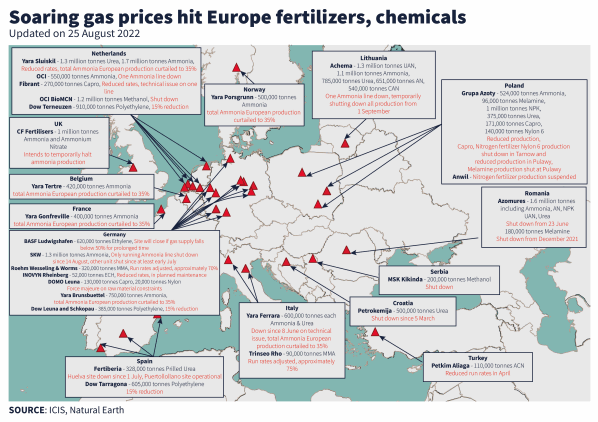

Stickstoffprodukte wie Düngemittel in die Höhe getrieben und mittlerweile zur Schließung vieler Ammoniak- bzw. Düngemittelfabriken in Europa geführt. 70 % der Produktionskapazität sind schon weggefallen. So musste kürzlich auch Litauens größte Düngemittelfabrik Achema den Betrieb aussetzen.

CEO Ramūnas Miliauskas kommentierte die Schließung wie folgt:

„In der derzeitigen Marktsituation sind die meisten westlichen Düngemittelhersteller gezwungen, ihre Fabriken zu schließen, und Achema ist da keine Ausnahme. Die Rekordpreise für Erdgas wirken sich direkt auf die Produktionskosten aus, und die Preise für unsere Düngemittel sind im Vergleich zur Produktion der US-amerikanischen und russischen Hersteller nicht mehr wettbewerbsfähig.”

Mit dem Ausfall der Düngemittelproduktion gehen nicht nur die Preise durch die Decke, sondern auch die Nahrungsmittelproduktion gerät zunehmend unter Druck. Welche Auswirkungen das haben kann, zeigt das Beispiel

Sri Lanka. Das Verbot des Einsatzes von Kunstdünger hat die Nahrungsmittelproduktion des Landes in nur einer Saison kollabieren lassen.

Die nachfolgende

ICIS Twitter-Grafik verdeutlicht das Ausmaß der geschlossenen Fabriken sehr anschaulich.

Glasindustrie: Leicht zerbrechlich ohne Gas

Auch die Glasindustrie ist auf das Erdgas angewiesen – und zwar in besonderem Maße. Glas wird in großen Schmelzwannen bei konstanten Temperaturen von bis zu 1.600 °C geschmolzen, damit es anschließend verarbeitet werden kann. Ein Abschalten der Produktionsanlage zwischendurch ist nicht vorgesehen – das geschmolzene Glas würde erstarren und die Wannen beschädigen, im schlimmsten Fall unbrauchbar machen.

Bei Kosten von 15 bis 20 Millionen Euro pro Wanne hätte daher selbst ein kurzzeitiger Ausfall der Gasversorgung katastrophale Folgen. Die Ersatzbeschaffung und das Wiederanfahren der Produktion würde mehrere Monate dauern. Eine kurzfristige Umstellung auf andere Energieträger ist bei einem Ausfall der Gasversorgung nicht möglich. Dafür sind mehrere Monate Vorbereitungszeit nötig.

Der explosionsartige Kostenanstieg macht es allerdings immer schwieriger, die Schmelzwannen wirtschaftlich zu betreiben und erweist sich für einige Unternehmen bereits als existenzbedrohend.

Glasprodukte haben eine enorme Bedeutung für viele Bereiche unseres Alltags und unserer Wirtschaft: Von Hohlgläsern für Nahrungsmittel und Kosmetikprodukte über Fensterglas und Spezialgläser für Technik und Wissenschaft bis hin zu Mineralfasern, aus denen Glas- und Steinwolle für die Wärmedämmung erzeugt wird.

Chemieindustrie: Das Herz der Wirtschaft

Für die chemische Industrie hat Erdgas eine zentrale Bedeutung als Rohstoff und Energieträger. Ohne Gas und Öl läuft nichts, und ohne die chemische Industrie läuft die Wirtschaft nicht. Die Branche produziert nicht nur systemrelevante Produkte wie Medikamente, Desinfektionsmittel oder Düngemittel, sondern liefert auch Vorprodukte für 96 Prozent aller in der EU hergestellten Waren.

Quelle: VCI

Kurzfristig ist in der Chemieindustrie das Erdgas kaum zu ersetzen. In den vergangenen Jahren wurde der Energieverbrauch im Zuge der

Dekarbonisierung der Chemieindustrie bereits deutlich gesenkt und vielerorts auf nachhaltige Technologien zur Energieerzeugung umgerüstet. Auch die Donauchem produziert an den Standorten in Niederösterreich und Kärnten eigenen Strom und ist nur in bestimmten Bereichen auf Gas angewiesen.

Schwierig ist der Ersatz von Erdgas aber in Bereichen, wo es als Rohstoff in chemischen Prozessen verarbeitet wird. In Zukunft könnten

Biogas und

Wasserstoff das Gas ersetzen, doch beides steht noch nicht in ausreichender Menge zur Verfügung.

Ein abrupter Stopp der Gasversorgung hätte katastrophale Auswirkungen auf die Versorgung mit lebenswichtigen Gütern.

Hubert Culik, Obmann des FCIO

Bereits eine Reduzierung der Erdgasversorgung auf weniger als 50 % des normalen Bedarfs würde in vielen Chemieunternehmen zu einer vollständigen Einstellung der Produktionstätigkeit führen. Damit verbunden wären nicht nur Engpässe bei energieintensiven Produkten wie Elektrolyse- und Stickstoffprodukten oder

Schwefelsäure. Auch unzählige nachgelagerte Branchen wären

von erheblichen Produktionsengpässen betroffen: Landwirtschaft, Lebensmittel, Automobil, Kosmetik und Hygiene, Bauwesen, Energiewesen, Pharma oder Elektronik - um nur einige anzuführen.

Papierindustrie: Kein Gas, kein Klopapier

Österreich gilt als „Papierland“. Die 23 heimischen Papier- und Zellstofffabriken produzieren pro Jahr fünf Millionen Tonnen Papier und zwei Millionen Tonnen Zellstoff. Gas wird in Papierfabriken für die Dampf- und Stromerzeugung benötigt, in den Zellstofffabriken als Start- und Stützbrennstoff. Dass die Papierindustrie so viel Gas braucht, liegt vor allem daran, dass der Papierbrei getrocknet werden muss, häufig mit Wärme, die aus Gas erzeugt wird.

Kurzfristig ist es technologisch nicht möglich, Gas durch einen anderen Brennstoff zu ersetzen. Bei einem Gasmangel oder zu hohen Gaspreisen könnten zunächst Teile der Produktion stillgelegt werden, wie dies voraussichtlich

in Kürze bei der Lenzing AG am Standort Heiligenkreuz im Südburgenland der Fall sein wird. Falls aber die Gasversorgung völlig zum Erliegen kommt, müssten alle Papierfabriken stillgelegt werden. Ein Notfallplan zur Umstellung auf Öl wurde wieder verworfen. Die Mengen an erforderlichem Öl, sprich alle zwei Stunden ein Tankwagen, sind logistisch nicht machbar.

© Austropapier

Ein Produktionsausfall hätte weitreichende Konsequenzen. Zahlreiche Produkte wären innerhalb kürzester Zeit nicht mehr verfügbar.

- Verpackungen für Grundnahrungsmittel wie Nudeln, Reis, Mehl, Salz, Brot, Eier, Milch und vieles mehr.

- Umverpackungen von Medikamenten und Arzneimitteln.

- Verpackungen für Paketdienste.

- Hygienepapiere aus Papier oder Zellstoff für die medizinische Versorgung oder für die Nutzung im Haushalt (Windeln, Toilettenpapier → Deutsche Papierindustrie warnt vor Engpass).

- Spezialpapiere für industrielle Prozesse (z.B. für den Einsatz bei der Lackierung von Fahrzeugkarosserien).

- Bücher, Zeitungen und Magazine.

Außerdem versorgen die Papierfabriken mit der selbst erzeugten Energie neben der eigenen Produktion auch Gebäude in der Umgebung mit 271 GWh Strom und 2.000 GWh Fernwärme. Diese ausgekoppelte Energie entspricht dem Strom- und Wärmebedarf von 100.000 Haushalten.

Stahlindustrie: Brot vor Stahl?

In der Stahlproduktion wird Gas als Brennstoff zur Erzeugung hoher Temperaturen genutzt. Außerdem kommt es, ebenso wie Roheisen, als Reduktionsmittel in verschiedenen Prozessschritten zum Einsatz. Eine Umstellung von Erdgas auf Erdöl oder Kohle ist nicht oder nur in sehr geringem Umfang möglich.

Wasserstoff als klimaschonende Alternative wird voraussichtlich erst um das Jahr 2030 einsatzfähig sein.

Stahl ist der Basiswerkstoff und Ausgangspunkt nahezu aller industriellen Wertschöpfungsketten. Ein Importstopp von Gas oder ein nicht mehr wettbewerbsfähiger Gaspreis würde nicht nur zu Produktionsstillständen führen (siehe

ArcelorMittal), sondern auch den Einbruch der Industrieproduktion in der EU verursachen.

Die Komplexität der Lieferketten wird häufig unterschätzt. Die Strategie „Brot vor Stahl“ ist im Ernstfall viel zu kurz gegriffen.

Hubert Culik, Obmann des FCIO

In Österreich beschäftigt die Stahlindustrie über 15.000 Menschen (Stand 2020). Dazu kommen noch tausende Arbeitsplätze von Industrien, die Stahl und Eisen als Werkstoffe benötigen. Die

Voestalpine, der größte Stahlproduzent Österreichs, hat sich auf das Worst-Case-Szenario bereits gut vorbereitet.

So bezieht das Unternehmen mittlerweile auch Gas aus Nordafrika und kauft Flüssiggas bei Terminals im Süden Europas zu. Außerdem sicherte sich der Konzern Gasreserven von 1,5 TWh, die u.a. in den RAG-Speichern Haag und Haidach eingespeichert wurden. Diese Menge reicht für drei Monate Vollbetrieb bzw. einen entsprechend längeren Teilbetrieb.

© Grobblech,

Voestalpine

Fazit: Wenn Gas ausbleibt, steht die Wirtschaft

Kurzfristige Alternativen für den Ausfall russischer Importe sind nicht verfügbar. Bereits 2021 wurde in einigen Branchen die Produktion gedrosselt, als der Gaspreis noch weit unter dem aktuellen Rekordpreis gelegen ist. Mittlerweile müssen einige Branchen die Produktion komplett aussetzen - mit drastischen Folgewirkungen in anderen Industrien.

Hunderttausende Arbeitsplätze wären bei weitreichenden Produktionsstillständen gefährdet. Das Heizen von Privathaushalten, die letztlich lediglich zu 20 % am Gas hängen, wird dann angesichts der wirtschaftlichen Verwerfungen nebensächlich. Die Abschaltung von Betrieben muss daher unbedingt vermieden werden.

www.donauchem.at

Weiterführende Links:

www.capital.de

www.donauchem.at

Weiterführende Links:

www.capital.de (Stand 29.09.2022)

Ausbau stockt: Hoffen auf ein Grüngas-Wunder (orf.at, Stand 09.01.2023)