Die chemische Industrie ist eine der großen Schlüsselindustrien bei der Umsetzung des Green Deals. Vor allem Green Tech-Technologien wie Batterien, Sonnenkollektoren, Windturbinen, Wasserstoff oder Gebäudeisolierungen sind auf die Innovationskraft der Chemieunternehmen angewiesen. Wie die Dekarbonisierung der Chemieindustrie erreicht werden kann, welche Herausforderungen auf diesem Weg zu meistern sind und wie realistisch die hochgesteckten Klimaziele derzeit sind, mehr dazu in diesem Beitrag.

Chemieindustrie im EU-Vergleich auf Platz 3

Bis zum Jahr 2050 will Österreich innerhalb der chemischen Industrie komplette Klimaneutralität erreichen. Schon heute gehören die heimischen Chemieunternehmen im internationalen Vergleich zu den Vorreitern bei klimafreundlicher Produktion. Durch spritsparende Leichtbaustoffe bei Autos oder energiesparende Wärmedämmung für Gebäude leistet die Branche bereits einen maßgeblichen Beitrag zur Dekarbonisierung.

Auch bei den Emissionen steht die Branche gut da. Im EU-Vergleich rangiert die Chemieindustrie Österreichs auf Platz 3 (Quelle:

Studie des Instituts für Industrielle Ökologie). Mit der Freisetzung von lediglich 37,46 Tonnen CO

2 pro Terajoule (TJ) liegt die Treibhausgasbelastung rund 60 Prozent niedriger als im EU-Durchschnitt (61 Tonnen CO

2/TJ).

Grafik:

CO2 Verbrauch in Tonnen pro Terajoule, FCIO

Auswirkungen der Dekarbonisierung auf die Chemieindustrie

Der Anteil der chemischen Industrie an den vom Menschen verursachten globalen CO

2-Emissionen beläuft sich auf etwa 9,5 Prozent. Mehr als die Hälfte davon entfällt auf die direkte Nutzung fossiler Kohlenwasserstoffe als Rohstoffe, die andere Hälfte dient als Energielieferant für die Branche.

Hohe Abhängigkeit von fossilen Brennstoffen

Der Faktor Energie macht bei der Herstellung verschiedener Produkte bis zu 75 Prozent der Produktionskosten aus. Die Beheizung und das Kühlen in chemischen Prozessen sind derzeit noch überwiegend abhängig von fossilen Brennstoffen, zum Beispiel in Form einer gasbefeuerten Kraft-Wärme-Kopplung. Eine nachhaltige Form wäre im Gegensatz dazu ein

dampfbetriebener, CO2-neutraler Wärmekreislauf, wie er im Industriepark Pischelsdorf bereits umgesetzt wurde.

Kein Erdöl - keine Petrochemikalien

Wird im Zuge der Energiewende kein Rohöl mehr in Raffinerien verarbeitet, fehlt es klarerweise an Basisprodukten wie Ethylen und Propylen sowie sämtlichen Folgeprodukten, die so wichtig für uns alle und die gesamte Menschheit sind (siehe

Flowchart der Chemie/Raffinerie). Die Folge davon werden extrem hohe Energiekosten und zunehmende Verknappungen sein - nicht nur bei chemischen Rohstoffen, sondern auch bei deren Folgeprodukten bis hin zu Produkten des Alltags.

Woher sollen also die chemischen Rohstoffe und die erforderliche Energie kommen, wenn wir vollständig auf den Einsatz fossiler Rohstoffe verzichten?

Bruttoinlandsverbrauch im Vergleich. In Österreich lag der Anteil erneuerbarer Energieträger am Bruttoinlandsverbrauch im Jahr 2020 bei 32,8 Prozent. Bis 2040 sollte dieser auf nahezu 100 Prozent steigen. Quelle:

Energie in Österreich, 2021

Dekarbonisierung erfordert wettbewerbsfähige Strompreise

Der Verzicht auf fossile Energiequellen bedeutet, dass wesentlich mehr günstige Energie aus alternativen Quellen benötigt wird. Wir sprechen hier von dem drei- bis fünffachen Energiebedarf für die Elektrifizierung der chemischen Prozesse. Für die Herstellung von Rohstoffen aus grünem Wasserstoff werden sogar acht- bis elfmal so viel an erneuerbaren Energien benötigt.

Alternativenergie hat geringeren Energiegehalt

Der hohe Energiebedarf im Zuge der Dekarbonisierung wird sich auch nicht durch technologische Innovationen signifikant verbessern lassen. Denn Kohlendioxid, Wasser und Luft verfügen über einen geringeren Energiegehalt als Erdgas, Erdöl oder Kohle - und sind daher schlechtere Ausgangsmaterialien für die Energieerzeugung. Auf diesen Rohstoffen basierende Verfahren sind somit wesentlich energieintensiver als jene, die auf Rohöl und Erdgas basieren.

60 Wasserkraftwerke für zusätzliche Ökostrom-Erzeugung

In einer 2018 veröffentlichten

FCIO-Studie gehen die Experten von einem zusätzlich erforderlichen Bedarf an Ökostrom von rund 60 TWh aus. Das entspricht 60 Wasserkraftwerken in der Größenordnung des Kraftwerks Freudenau oder dem Strombedarfs Österreichs in einem Jahr. Eine vernünftige Kreislaufwirtschaft könnte diesen Bedarf jedoch auf 30 TWh halbieren, so die

Ergebnisse der FCIO-Folgestudie.

Der Bau von alternativen Stromerzeugern alleine greift aber zu kurz. Derzeit fehlt es in Österreich immer noch an der Infrastruktur und den Netzen, um grünen Strom dorthin zu verteilen, wo er gebraucht wird. Nur eine gesamtheitliche Sicht der Energiewende kann letztlich erfolgreich sein. In diesem Sinne müssen natürlich auch andere Industriebereiche wie z. B. Wohn- und Straßenbau entsprechende Ziele setzen.

Primärenergieerzeugung im Vergleich. International betrachtet liegt der Anteil Österreichs an der gesamten EU-Primärenergieerzeugung bei 2,0%, an der Erzeugung erneuerbarer Energien bei 4,6%. Quelle: Energie Österreich 2021

Recycling und Technologiemix für CO2 neutrale Chemie

Große Potentiale zur Dekarbonisierung in der Chemieproduktion würden laut der FCIO-Folgestudie in der Verwendung von

erneuerbarem Wasserstoff, dem Einsatz von bio- und abfallbasierten Rohstoffen und vor allem in einer massiven Forcierung von Kunststoffrecycling liegen. Um die Potentiale der Kreislaufwirtschaft nutzen zu können, ist allerdings die gesetzliche Anerkennung des Kunststoffrecycling als Klimaschutzmaßnahme sowie die rechtliche Gleichstellung von chemischem Recycling erforderlich.

1. Reduzierung des Strombedarfs durch Technologiemix

Die Branche könnte ihren Kohlenstoff aus CO

2-Abgasen und Biomasse beziehen, den benötigten Wasserstoff mittels Elektrolyse aus Wasser gewinnen sowie die Dampferzeugung verstromen. Durch diesen Technologiemix lassen sich bis 2040 in Österreich jährlich bis zu 2,4 Mio. t CO

2 einsparen und die zusätzlich notwendige Energie von 60 auf 30 TWh halbieren.

Insbesondere der Einsatz von erneuerbarem Wasserstoff spielt dabei eine signifikante Rolle. So könnte etwa Ethylen oder Propylen zur Herstellung von Kunststoffen aus einer Mischung von CO

2 und erneuerbarem Wasserstoff hergestellt werden. Das dafür erforderliche CO

2 kann aus industriellen Prozessen oder Kraftwerksabgasen abgeschieden werden.

Im Rahmen eines

zukunftsträchtigen Projekts arbeiten bereits mehrere heimische Unternehmen an der großtechnischen Verwendung von CO

2 als Ressource für die Fertigung von Olefinen, Kraftstoffen und hochwertigen Kunststoffen.

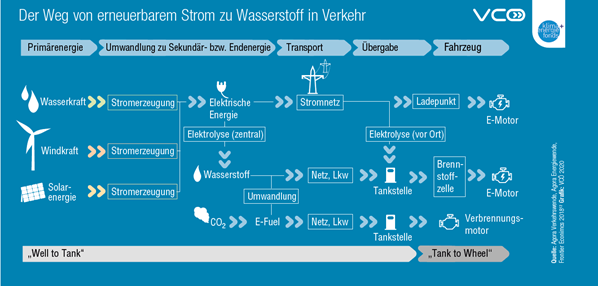

Grafik: Erzeugung erneuerbaren Wasserstoffes am Beispiel Verkehr © VCÖ

2. Biobasierte Rohstoffe

Der verstärkte Einsatz von biobasierten Rohstoffen bei der Herstellung chemischer Stoffe stellt einen weiteren wichtigen Baustein klimaneutraler Produktion dar. Dabei ist allerdings das Thema der

Flächenkonkurrenz, insbesondere in Hinblick auf die Lebensmittelproduktion, zu beachten, welches in Österreich zunehmend an Relevanz gewinnt.

Ebenfalls braucht es noch die globale Infrastruktur für die Endverwertung bzw. Kompostierung von biobasierten Kunststoffen. Dafür sind bestimmte Temperaturen und Sauerstoffgehalte notwendig, die auf einer klassischen Müllhalde nicht gegeben sind. Falsch entsorgt verrotten Biokunststoffe nur sehr langsam und produzieren das Treibhausgas Methan, welches noch schädlicher als CO

2 ist.

Asien pfeift auf die Dekarbonisierung der Industrie

Die Länder der EU, und damit zu einem kleinen Teil die chemische Industrie Österreichs, tragen in Summe nur etwa 10 Prozent zu den globalen Treibgasemissionen bei. Die Tendenz ist dabei bereits jetzt sinkend - vor allem durch freiwillige Vorleistungen einzelner Länder, Industrien oder Branchen.

Ein klimapolitischer Alleingang der EU wird im globalen Kontext aber nicht viel dazu beitragen, unsere Welt wieder lebenswerter zu machen. Alleine die drei größten Verursacher China, USA und Indien sind inzwischen für etwas mehr als die Hälfte der weltweiten CO

2-Emissionen verantwortlich.

Vor allem China bremst die EU klimapolitisch massiv aus. Nach Angaben des

Global Energy Monitors gingen 2020 neue Kohlekraftwerke mit einer Leistung von 38,4 Gigawatt in Betrieb – das ist dreimal so viel wie der gesamte Rest der Welt zusammen! Mehr als 600 weitere Kohlekraftwerke sind in China, Indien, Indonesien, Japan und Vietnam geplant. Insgesamt sollen sie 300 Gigawatt Energie erzeugen - das entspricht der gesamten Erzeugungskapazität Japans.

Kohlekraftwerke sollten eigentlich bald der Vergangenheit angehören.

Wer soll die gigantischen Kosten der Energiewende tragen?

Unter diesen Rahmenbedingungen wird die Energiewende in Europa ganze Industrien schwer belasten, den globalen CO

2-Ausstoß aber nicht merklich verringern. Um bis 2050 klimaneutral zu werden, müsste die chemische Industrie jährlich rund 580 Millionen Euro investieren. Gleichzeitig ist mit höheren Produktions- und Netzinfrastrukturkosten zu rechnen, die Österreichs international ausgerichtete Chemieunternehmen in ihrer Wettbewerbsfähigkeit massiv beeinträchtigen würden.

Hohe Wellen schlug kürzlich auch der

Bank of Amerika (BofA) Global Research Report mit einer Berechnung der möglichen Kosten für die Umsetzung der Maßnahmen und Ziele der Klimawende – und die sind gigantisch:

150 Billionen US-Dollar an neuen Kapitalinvestitionen wären notwendig, um über 30 Jahre eine „Netto-Null“-Welt zu erreichen. Das würde jährliche Investitionen von etwa 5 Billionen US-Dollar bedeuten - was dem Doppelten des aktuellen globalen BIP entspricht. Wer soll diese enormen Summen bezahlen? Private Investoren werden es vermutlich nicht sein.

Quelle:

„Transwarming” World: Net Zero Primer, BofA Global Research

Energiekrise: Das Ende der Energiewende?

Während also die Energiewende in der EU gerade begonnen hat und andere Länder massiv ihre fossile Energiegewinnung ausbauen, steckt Europa in einer beispiellosen Energiekrise. Die Preisanstiege haben inzwischen nicht nur einige Energieversorger in die Pleite getrieben, sondern auch zu

erheblichen Produktionseinschränkungen in der chemischen Industrie wie auch anderen energieintensiven Branchen geführt.

Europa hat es offenbar versäumt, die Energieversorgung durch erneuerbare Energie sicherzustellen, bevor Erdgasförderfelder, Atomkraftwerke und Kohlefabriken geschlossen wurden. Der Ausstieg aus fossilen Energieträgern, die erzwungene Abschaltung aller Atomkraftwerke (in Deutschland) steht der steigenden Stromnachfrage aufgrund der Energiewende (Elektroautos, Wärmepumpen, etc.) entgegen.

Aus aktueller Sicht wird sich die Situation der Energieversorgung in Europa zuspitzen und die Strompreise in die Höhe schnellen lassen. Wenn die EU nicht gegensteuert, wird als Folge die Akzeptanz für neue Klimaschutzmaßnahmen weiterhin schwinden – was wiederum den „Green Deal“ gefährdet.

Europa braucht Balance zwischen Green-Deal und Fossil-Deal

Die Dekarbonisierung der Industrie kann nicht im Alleingang europäischer Länder gelöst werden. Es braucht keine österreichische, keine europaweite, sondern eine globale Trendwende und eine Umkehr aus alteingefahrenen Bahnen. Die Herausforderung muss es sein, eine vernünftige Balance zwischen „Green-Deal“ und „Fossil-Deal“ zu finden.

Um Energieversorgungssicherheit gewährleisten zu können, müsste aber einiges an der europaweiten Industriepolitik gedreht werden:

- Deckelung/Begrenzung von Ökostromabgaben, um Energiekosten für Betriebe zu begrenzen.

- Das Heranführen von erneuerbaren Energien an die Marktreife.

- Ökostrom-Fördersysteme.

- Netzausbau und Modernisierung der Energieinfrastruktur. Das EU-Stromnetz in seiner aktuellen Form entspricht nicht den Anforderungen unserer Zeit.

- Industrielle Eigenstromerzeugung als Beitrag zur Versorgungssicherheit mit Energie.

- Verstärkte Nutzung von Biomasse.

Große Unternehmen und Multinationals der chemischen Industrie wie BASF, DOW, Shell, ExxonMobil, Chevron

arbeiten bereits daran, ihre Unternehmen für die Zukunft fit und ebenfalls klimaneutral zu gestalten. Optimistischerweise wird dies allerdings erst ab 2050 auch Realität werden können.

Fazit: Dekarbonisierung der chemischen Industrie

Die chemische Industrie nimmt eine bedeutende und führende Rolle auf dem Weg zur Klimaneutralität ein. Auf Basis einer Kreislaufwirtschaft in Kombination mit entsprechenden Technologien ist die Dekarbonisierung der chemischen Industrie durchaus bis zum Jahr 2050 in Österreich zu erreichen. Dafür braucht es aber geeignete rechtliche Rahmenbedingungen, Investitionsförderungen und vor allem günstigen Strom aus alternativen Quellen. Gleichfalls gilt es, die Balance nicht aus den Augen zu verlieren, um weiterhin im globalen Wettbewerb konkurrenzfähig zu bleiben.

www.donauchem.at

Quellen und Sammlung weiterführender Information:

Perspektiven zur Dekarbonisierung der chemischen Industrie

www.donauchem.at

Quellen und Sammlung weiterführender Information:

Perspektiven zur Dekarbonisierung der chemischen Industrie, Institut für industrielle Ökologie (2018)

Die chemische Industrie auf dem Weg zur Klimaneutralität, Institut für industrielle Ökologie (2020)

Integration erneuerbarer Energien durch Sektorkopplung: Analyse zu technischen Sektorkopplungsoptionen, Umweltbundesamt (2019)

Net Zero by 2050: A Roadmap for the Global Energy Sector (2021)

Global Research Report „Transwarming World“ - Net Zero Primer - Bank of America (2021)

Energie in Österreich - Zahlen, Daten, Fakten - Bundesministerium für Klimaschutz, Umwelt, Energie, Mobilität, Innovation und Technologie (2021)

climApro:Factsheet Potenzialanalyse veränderter Produktionsstrukturen in der österreichischen chemischen Industrie für globalen Klimaschutz und ihre monetären Auswirkungen - FCIO

Chemie unter Strom - zeitung.faz.net - 13.Jan. 2022