Vor wenigen Tagen hat Russland angekündigt, Exporte von Produkten und Rohstoffen bis zum 31. Dezember zu verbieten. Was davon betroffen sein wird, ist derzeit noch unklar. Ersten Einschätzungen zufolge könnte das Exportverbot für Öl, Gas, Getreide, Metalle und eine Reihe wichtiger Rohstoffe gelten. Sollte dies tatsächlich so eintreten, wären damit gravierende Auswirkungen auf die Energie- und Rohstoffversorgung in Österreich und Europa verbunden.

Russland ist größter Erdgaslieferant der EU

Europa ist von Russlands Öl- und Gasexporten in hohem Ausmaß abhängig. Angesichts der Tatsache, dass die Energiepreise in der EU im vergangenen Jahr bereits von 20 Euro auf 180 Euro pro Megawattstunde gestiegen sind, könnte der Wegfall dieser Gas- und Ölimporte eine schwere Belastung für Europa bedeuten.

Österreich bezieht 80 Prozent seines Erdgases aus Russland

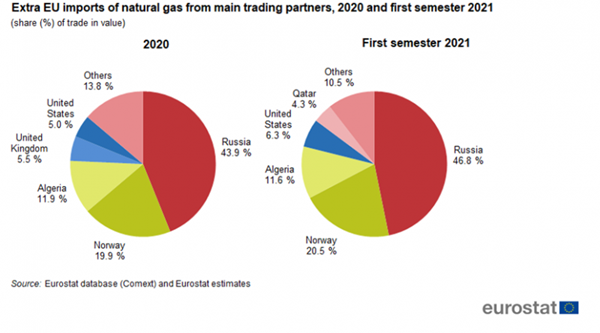

Russland war sowohl im Jahr 2020 als auch im ersten Halbjahr 2021 der größte Erdgaslieferant für die EU. Laut

Eurostat stammen im Jahr 2020 rund 44 Prozent der europäischen Erdgasimporte aus Russland. Im ersten Halbjahr 2021 stieg dieser Anteil auf fast 47 Prozent. Österreich bezog 2021 laut

WKO rund 80 Prozent seines Erdgases von Russland.

Industrie und Kraftwerke als größte Gasverbraucher

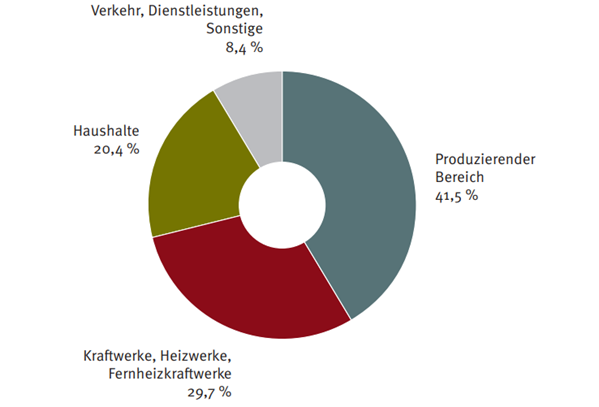

Hauptverbraucher von Gas in Österreich war 2020 mit einem Anteil von 41,5 Prozent der produzierende Bereich. Dieser Sektor verwendet Erdgas zur Erzeugung von Prozesswärme oder als Rohstoff in der Produktion. 29,7 Prozent der gesamten Gasnachfrage wurde 2020 im Umwandlungsbereich für die Strom- und Fernwärmeerzeugung eingesetzt. Bei den Haushalten (20,4 Prozent der Gasnachfrage) stehen die Anwendungen Raumheizung, Warmwasserbereitung und Kochen im Vordergrund.

Quelle:

Zahlenspiegel Gas und Fernwärme 2021

Österreich importiert 10 Prozent seines Erdöls aus Russland

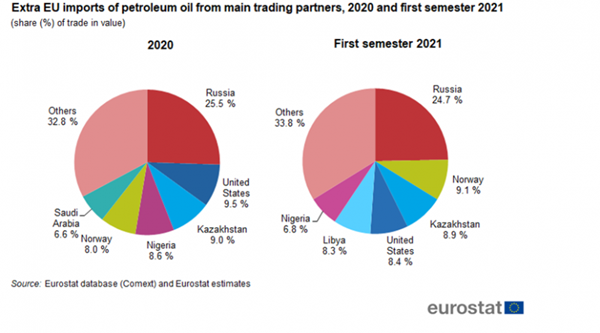

Bei Erdöl ist Russland mit einem EU-Importanteil von rund 25 Prozent weniger dominant als bei Erdgas, aber immer noch weit vor dem zweitgrößten Lieferanten Norwegen. Österreich bezog im Zeitraum 2010 bis 2020 insgesamt 7,84 Millionen Tonnen Rohöl aus Russland, das entspricht etwa 10 Prozent aller Rohölimporte.

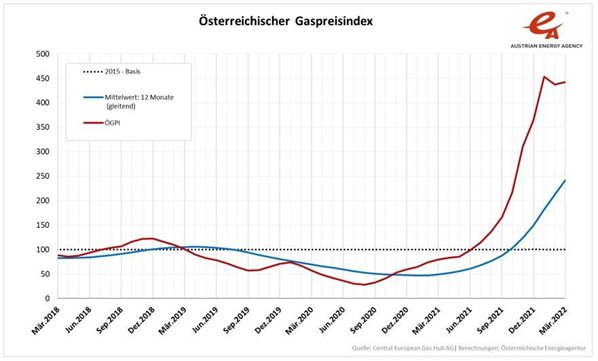

Erdgas-Preis schnellt um 60 Prozent in die Höhe

Schon vor der Ukraine-Krise hatte der Gaspreis deutlich zugelegt. Ende 2021 lag der Preis bei rund 148 Euro je Megawattstunde, im langjährigen Mittel bewegte er sich zwischen zehn und 25 Euro. In der ersten Märzwoche 2022 erreichte der Gaspreis erstmals die Marke von 200 Euro je Megawattstunde.

Die Befürchtung der Händler, dass Gaslieferungen nach Europa unterbrochen werden könnten, ließen den Gaspreis nur wenige Tage später erneut um 60 Prozent in die Höhe schnellen. Am niederländischen Handelspunkt TTF (Title Transfer Facility) wurde eine Megawattstunde zeitweilig für 345 Euro gehandelt (7.3.2022).

Der Österreichische

Gaspreisindex (ÖGPI) liegt aktuell im Vergleich zu März 2021 um 455,5 Prozent höher.

Auch beim Erdöl sind politische Entscheidungen und Befürchtungen maßgebliche Treiber der Teuerungsrate. Per 10.3.2022 beträgt der Preis für ein Barrel (159 Liter) der Nordseesorte Brent 113,29 US-Dollar, der Preis für ein Fass der US-Sorte West Texas Intermediate (WTI) bei 109,90 Dollar. Erste Auswirkungen spiegeln sich bereits bei Benzin und Spezialbenzinen mit einem Preisanstieg von 40 Prozent.

Flüssiggas per Tankschiff als Alternative?

Die weitgehende Versorgung Europas per LNG-Tanker ist logistisch und wirtschaftlich derzeit kaum machbar. LNG ist mit enormen Kosten verbunden und Europa muss mit anderen gasverbrauchenden Regionen um knappe Lieferungen konkurrieren.

In Europa liegt der Engpass vor allem bei der Anzahl der Flüssiggas-Terminals. Diese sind notwendig, um das Flüssiggas wieder in einen gasförmigen Zustand zu versetzen und in das Gasnetz einzuspeisen. Einer ICIS-Studie zufolge könnten selbst bei kompletter Auslastung aller verfügbaren Flüssiggas-Terminals aktuell nur 40 Prozent des Gasbedarfs Europas über LNG gedeckt werden, falls russische Erdgasimporte wegfallen.

Die Einfuhr von mehr Gas aus Übersee ist somit aufgrund der begrenzten Transport- und Umwandlungskapazitäten keine wirkliche Option. Außerdem könnten verstärkte Flüssiggas-Importe laut Experten der Commerzbank mögliche Ausfälle russischer Pipeline-Lieferungen ohnehin nicht ausgleichen, da Russland aktuell rund ein Fünftel der LNG-Importe der EU stellt. Diese Volumina müssten bei einem eventuellen Lieferembargo zusätzlich kompensiert werden.

Wirtschaftliche Störungen in energieintensiven Industrien

Für energieintensive Branchen wie die Chemieindustrie könnte die Ukraine-Krise äußerst schwierig werden, sollte Gas in Österreich und in Europa knapp werden oder sich erheblich verteuern. Zwar fließt russisches Gas derzeit noch in großen Mengen nach Europa, eine Reduktion oder ein Stopp von Lieferungen kann aber nicht mehr ausgeschlossen werden.

Der Preisschock bei Gas ist inzwischen ein Riesenproblem für die Chemieindustrie. Die Branche ist ohnehin schon durch ein historisch extrem hohes Erdgas-Preisniveau und steigende Stromkosten belastet. Bereits 2021 wurde in einigen Branchen die Produktion gedrosselt, als die Gaspreise noch weit unter den aktuellen Preisen gelegen hatten. Ein fortgesetzter Anstieg der Energiepreise könnte dazu führen, dass Unternehmen die Produktion aus Kostengründen nicht nur drosseln, sondern komplett aussetzen müssen.

Erste Unternehmen drosseln bereits Produktion

Erste Produktionsrückgänge sind bereits bei Prozessen festzustellen, die stark von Erdgas abhängig sind. Das betrifft aktuell vor allem Elektrolyseprodukte, Schwefelsäure und Stickstoffprodukte:

1. Elektrolyseprodukte

Die Erzeugung stromintensiver Elektrolyseprodukte wie Natronlauge und Kalilauge ist durch die Koppelung von Gas- und Strompreis indirekt von den steigenden Energiekosten für Gas betroffen.

2. Schwefelsäure

Die Herstellung von Schwefelsäure erfolgt im energieaufwendigen

Doppelkontaktverfahren. Als einer der wichtigsten Rohstoffe in der chemischen Technologie würde sich eine weitere Verknappung gravierend auf zahlreiche Industrien auswirken.

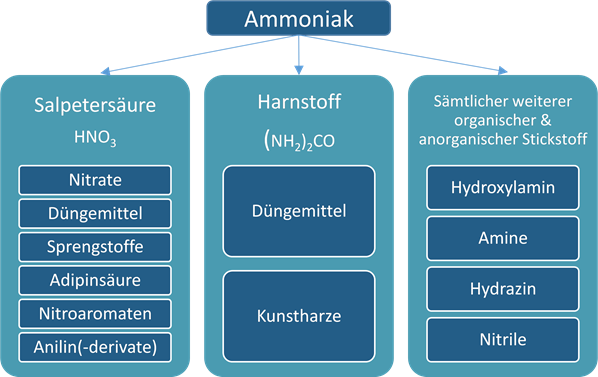

3. Stickstoffprodukte

Ammonium als Basis von

Stickstoffprodukten ist im Herstellungsprozess direkt von Erdgas abhängig. Erste Preisanstiege bei Stickstoffprodukten von mehr als 40 Prozent sind bereits zu verzeichnen. Sollte es als Folge der hohen Gaspreise zu Produktionsausfällen bei der Ammonium- und Harnstoffproduktion kommen, wirkt sich dies unmittelbar auf die Herstellung von AdBlue aus. Weiter gedacht, würde es zu einer massiven Einschränkung des LKW-Verkehrs kommen.

Ohne Stickstoffprodukte könnten auch keine Düngemittel mehr produziert werden. Der steigende Erdgaspreis führt bereits jetzt zu einer Reduzierung der Düngemittelproduktion und lässt die Preise von Nahrungsmitteln steigen. In Kombination mit dem

Phosphorsäure-Mangel bedeutet dies eine zusätzliche Belastung für die Düngemittelindustrie.

Hinzu kommt, dass die EU etwa 30 Prozent ihrer Düngemittel aus Russland bezieht. Russland ist einer der weltweit wichtigsten Exporteure von Düngemitteln und wichtiger Vorprodukte. So werden in Russland 23 Prozent des weltweiten Ammoniaks und 14 Prozent des Harnstoffes hergestellt Außerdem fördert Russland 21 Prozent der weltweiten Kalisalze.

Feedstock für petrochemische Produktion in Europa gefährdet

Die Ukraine-Krise hat nicht nur steigende Energiepreise zur Folge, sondern könnte auch die petrochemische Produktion in Europa ernsthaft bedrohen. Das derzeit diskutierte Embargo von Öl und Gas aus Russland würde die Raffinerien in Europa hart treffen. Mehrere Pipelines wären gleichzeitig davon betroffen.

1. Gas-Pipelines

Mit einem Schlag kämen die Gaslieferungen von mindestens drei maßgeblichen Gas-Pipelines (Jamal Europa, Nord Stream 1, Bratstvo/Urengoj-Uzhgorod) zum Erliegen. Möglicherweise würde es auch zum Stillstand der Progress- und Turkish Stream-Pipeline kommen.

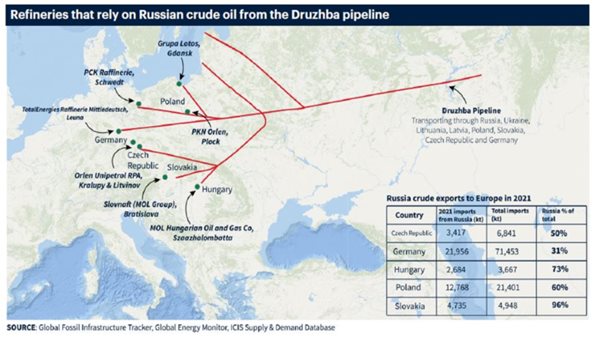

2. Ölpipeline

Die Rohöllieferungen über die Druschba-Pipeline wären im Falle eines Embargos ebenfalls unterbrochen.

3. Raffinerien stehen im Falle eines Embargo stil

Sämtliche Raffinerien in Ungarn, der Slowakei, der Tschechischen Republik, Polen, Ostdeutschland (Leuna) und Österreich erhielten keinen Feedstock mehr für die Erzeugung von Petrochemikalien aus Erdgas und Erdöl. Die Versorgung großer Teile Europas mit Basischemikalien wäre damit massiv unter Druck. Gleichzeitig würden mit einem Embargo vermutlich auch alle Grundchemikalien wie Anorganika und Petrochemikalien wegfallen, die aus Russland importiert werden.

Keine Petrochemikalien – keine Chemieproduktion

Das Kappen der Ergas- und Erdöllieferungen aus Russland würde sich unmittelbar auf die Verfügbarkeit von Benzinen/Hydrocarbons und zahlreiche weitere organische Synthesegrundstoffe auswirken. Das wäre aber nur der Beginn, denn fast alle chemischen Prozesse basieren heute auf petrochemischen Grundstoffen (siehe:

Flowchart Petrochemie).

1. Engpässe bei Olefinen

Insbesondere bei Ethylen und Propylen ist mit Einschränkungen zu rechnen. Laut

ICIS-Daten sind für 2022 voraussichtlich 2,79 Mio. Tonnen Ethylen (11 Prozent der gesamten europäischen Kapazität) und 2,34 Mio. Tonnen Propylen (12 Prozent der gesamten europäischen Kapazität) auf Raffinerien entlang der Druschba-Pipeline angewiesen. Obwohl einige alternative Rohölquellen beschafft werden könnten, ist es unwahrscheinlich, dass normale Betriebsniveaus aufrechterhalten werden könnten.

Ethylen und Propylen sind wichtige Basisprodukte für chemische Reaktionen. Ein Engpass würde alle weiteren Streams beeinflussen, z.B.:

- Ethylenoxide – Ethanolamine – Glykole – Polyesters – alle Solvents

- Styrol-Monomer – Polystyrol (Styropor)

- Acrylnitril – Rubbers/Plastics,…

- Cumol – Phenol – Aceton – alle Folgeprodukte

- Propylenoxid – Glykole – alle Solvents

- Butadiene – Rubbers/Plastics

Olefine sind essentiell für die Produktion von Kunststoffen, Düngemitteln, Beschichtungen, Bekleidungen, Verpackungen, Reinigungsmitteln, Arzneimitteln, Treibstoff und vielem mehr.

2. Engpässe bei Aromaten

Ebenso wären alle Aromaten wie Benzol, Toluol und Xylol sowie deren Folgeprodukte von einer Stilllegung der Raffinerien betroffen. Aromaten dienen zur Erzeugung von Polymeren, Kunstharzen und Polyester und werden z.B. auch für die Produktion von Elektronik, Beschichtungen, Sportutensilien oder Textilien verwendet.

Fazit: Auswirkungen des Ukraine-Konflikts

Die Chemieindustrie in Österreich und Europa muss sich aufgrund der aktuellen Entwicklungen auf weiter steigende Gaspreise einstellen. Im Falle eines Stopp der Gas- und Öllieferungen aus Russland hat die Industrie vor allem drei Probleme:

Zum einen würden die Gaspreise vermutlich extrem ansteigen, womit es sich für viele Unternehmen nicht mehr lohnen würde, zu produzieren. Zum anderen könnten die europäischen Raffinerien nicht mehr produzieren, wodurch ein Engpass wichtiger Basischemikalien entstehen würde. Außerdem kann es zu staatlich verordneten Zwangsabschaltungen zugunsten der Privathaushalte kommen. Ein russisches Exportverbot von Düngemitteln und wichtigen Chemikalien wie Ammonium und Harnstoff würde zudem vor allem die Landwirtschaft treffen und Nahrungsmittelpreise erneut ansteigen lassen.

www.donauchem.at

Weiterführende Links:

Raus aus dem Gas - orf.at 14.03.2022

Weltweite Düngemittelkrise befürchtet - orf.at 20.03.2022

www.donauchem.at

Weiterführende Links:

Raus aus dem Gas - orf.at 14.03.2022

Weltweite Düngemittelkrise befürchtet - orf.at 20.03.2022